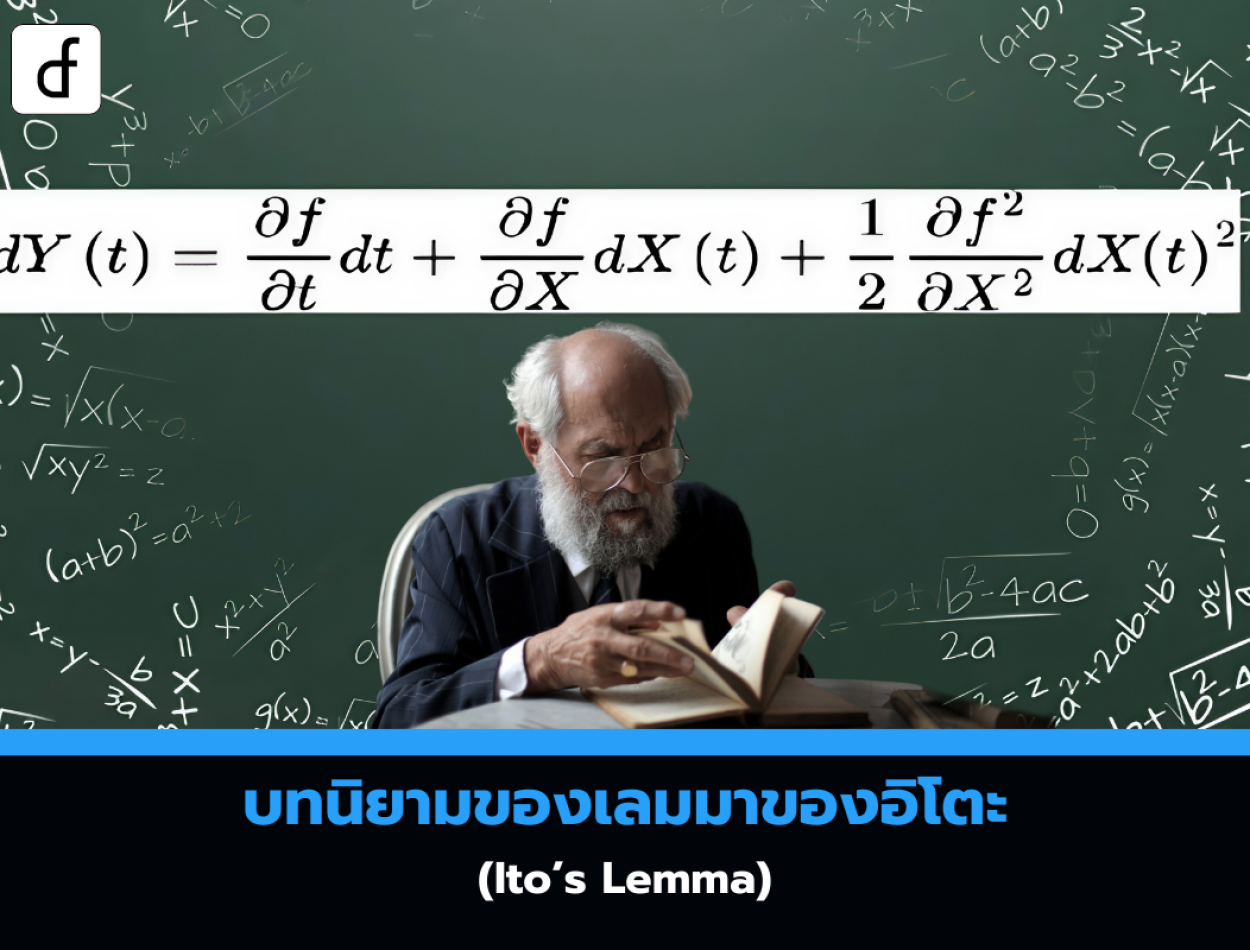

Definition of Itos Lemma

2025-05-06 09:34:54

Ito's Lemma is a key component in the Ito Calculus, used to determine the derivative of a time-dependent function of a stochastic process. It performs the role of the chain rule in a stochastic setting, analogous to the chain rule in ordinary differential calculus. Ito's Lemma is a cornerstone of quantitative finance and it is intrinsic to the derivation of the Black-Scholes equation for contingent claims (options) pricing.

It is necessary to understand the concepts of Brownian motion, stochastic differential equations and geometric Brownian motion before proceeding.

The Chain Rule

One of the most fundamental tools from ordinary calculus is the chain rule. It allows the calculation of the derivative of chained functional composition. Formally, if W(t) is a continuous function, and:

Then the chain rule states:

When f has t as a direct dependent parameter also, we require additional terms and partial derivatives. In this instance, the chain rule is given by:

In order to model an asset price distribution correctly in a log-normal fashion, a stochastic version of the chain rule will be used to solve a stochastic differential equation representing geometric Brownian motion.

The primary task is now to correctly extend the ordinary calculus version of the chain rule to be able to cope with random variables.

Ito's Lemma

Theorem (Ito's Lemma)

Let B(t) be a Brownian motion and W(t) be an Ito drift-diffusion process which satisfies the stochastic differential equation:

If

With

Reference: Ito's Lemma

From https://www.quantstart.com/articles/Itos-Lemma/

Leave a comment :

Recent post

2025-01-10 10:12:01

2024-05-31 03:06:49

2024-05-28 03:09:25

Tagscloud

Other interesting articles

There are many other interesting articles, try selecting them from below.

2025-03-24 02:41:04

2024-12-16 11:31:42

2025-01-29 02:50:10

2024-01-05 03:55:22

2024-10-18 02:43:35

2023-10-30 04:35:37

2025-03-19 10:34:30

2023-10-06 01:28:23

2024-08-13 01:06:54